A left-leaning friend of mine who was big into economics and business (as it was, well, his business) once described our current financial system as having organically and piecemeal emerged bit by bit into a rat’s nest of tangled protocols. And that now it’s ended up as a Gordian knot strangling us to death, but that cutting will kill us.

And that now it’s ended up as a Gordian knot strangling us to death, but that cutting will kill us.

so why wait?

Now you sound like him. But his was an advocacy based less on “Let’s get it over with” and more “I’ve had a brick on the pedal for years and I’ve been waiting to find a good cliff to drive off of”

Now you know why econ forecasting as an industry has such a high rate of liver failure. No one can stay sober when both options result in a complete unwinding of society. There are no good ways forward. There’s, likely, no way forward.

I mean when we can get of all global debt by paying it to the actual debtors, we could then finally move the economy forward into something more sustainable.

No one, except maybe complete unhinged psychopaths, wants to be responsible for billions of deaths, even those who talk/write so lightly of it

I don’t believe the current system (by that, I just mean the institutions controlling currency) is what’s killing us. The economic policies of different governments are the ones killing us.

I am a strong believer in leftist policies. However, I also believe that we don’t have a better system than markets. The presence of markets requires the presence of Keynesian economics if we want to avoid boom-bust cycles.

That being said, do I think Keynesian economics will continue to exist decades in the future? No. One of the biggest flaws of this system is that monetary policies require a lot of time to have an effect on the economy. This huge ping difference understandably introduces many issues.

There are better ways to control the amount of money in circulation (like fluctuating transaction fees) whose effects can be a lot more immediate. However, they require all money to be electronic.

Immediate impact is not necessarily a good thing. A lot of our economy is built on predictability. Imagine going to use your credit card, and something costs more because the fee jumped yesterday, and might be less tomorrow. Banks would build in bigger fees to avoid the uncertainty. Because people want certainty.

Changes in transaction fees wouldn’t be so drastic though. As you can make tens of thousands of corrections per year (compared to a couple in the current system), changes wouldn’t affect you so much.

The whole history of compound interest is quite fascinating. Early arguments for it are that seeds and livestock are capable of reproducing and multiplying themselves. If I lend you a handful of seeds and a year later you give back the exact same size handful, I have lost a whole year’s production I could have gotten out of those seeds.

Furthermore, assuming you actually planted the seeds instead of tucking them away in a drawer somewhere before giving them back later, those seeds produced a crop for you. This crop you could harvest and sell or feed yourself or your family or livestock. You could even save seeds from the harvest and pay me back the handful while keeping even more seeds for yourself. So by lending you seeds interest-free I’m essentially giving you a gift of harvest potential as well even more seeds in the future, at my own expense. Thus is the time value of money.

From this initial seed of an idea grows a huge amount of the financial system.

Yeah, very organic and reasonable growth into a gigantic and incomprehensible beast. Fascinating, but, kind of wish I didn’t have to live through it.

Was there a time in the past you would have preferred? I grew up in the 90s and I really miss that time period but I don’t think I’d prefer to live at any time before the 20th century over now. As complex and difficult as life is right now, other time periods tended to be much nastier for various reasons.

I could skip a good 200 years into the future when hopefully things have already fallen apart and been put back together.

I admire your optimism! I could easily see us living in a Mad Max situation in 200 years.

One thing I never see people talking about with fossil fuels is that they were a one shot deal in earth’s history, never to be repeated. If global civilization completely collapses (particularly the industrial base) then attempting to start over without fossil fuels could leave us stuck in a 17th century type situation for an extremely long time.

The problem is that renewables just don’t bootstrap. They require huge amounts of minerals which we’ve only been able to mine and process using heavy equipment and manufacturing powered by fossil fuels. Trying to do all that from a minecart-horse-and-pickaxe level of technology isn’t going to work out.

The other major factor is of course all the really easy mineral sources are gone too. Instead of mining directly from the ground we’d be salvaging scrap materials from the mountains of disposable electronics we’re producing right now. That’s where things really start to look like Mad Max.

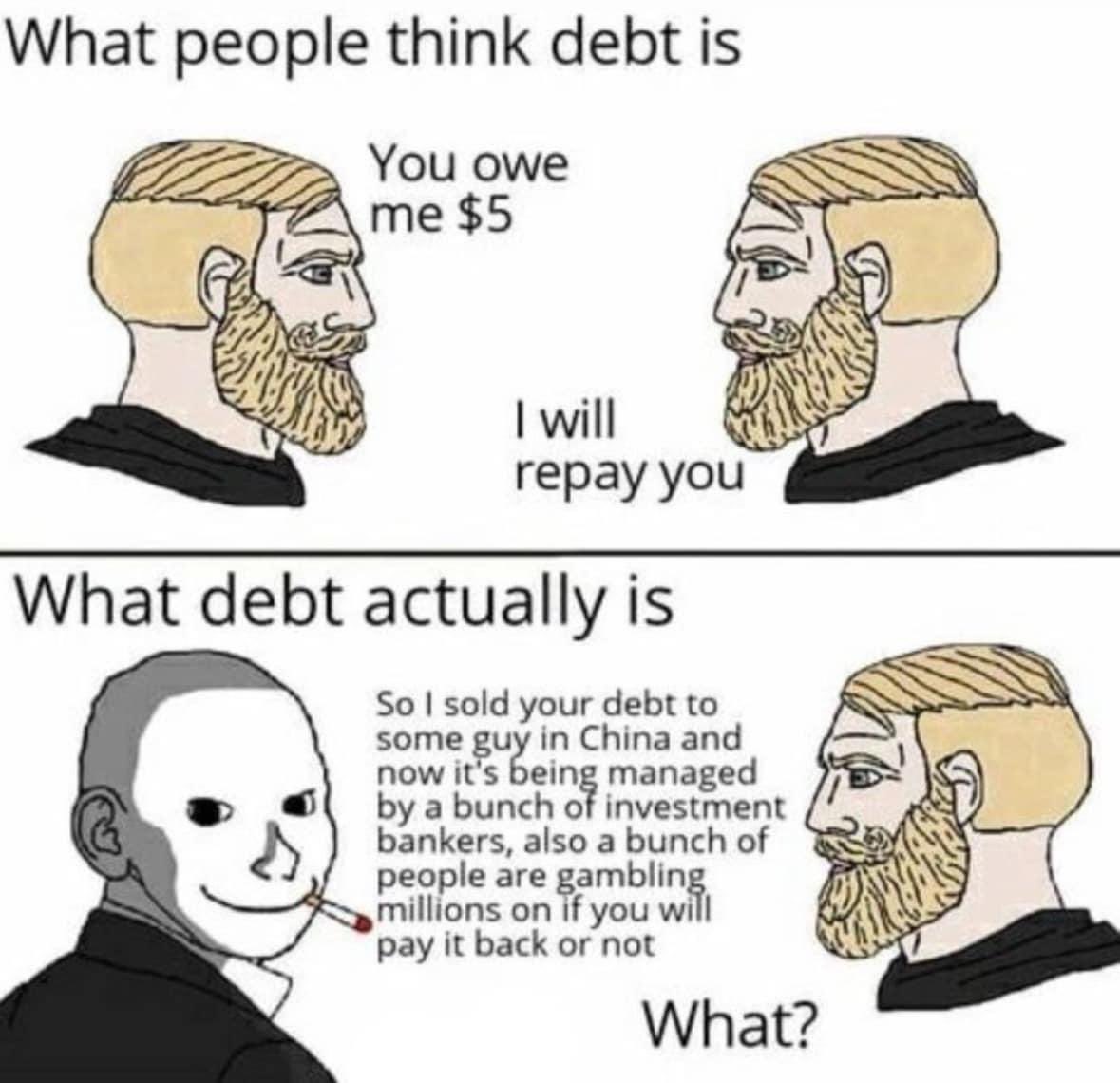

What it actually is:

We’ve given big, privately owned banks the right to create money out of thin air.

They lend it to you for a while, if you can prove that there’s no risk involved.

You still have to pay them back a lot more than you got.

Once you’ve given the money back, it disappears.

The banks keep the interest, though. And can use it to create 10x more money out of thin air.Man, if it were just this then banks would be pretty stable.

The problem is banks don’t just lend and receive money, they invest. And they invest in everything. And they take super risky bets.

This is what caused the banking collapse of 2008 and what caused the death of SVB and a few other banks.

Your bank doesn’t just hold your money and debt, if you rent it almost certainly owns a peice of the company managing your property. It owns crypto assets. It has shares of startups. And it uses those assets to get more money to create more debt.

Dobb Frank was created to stop some of this, but unfortunately it’s been effectively repealed already.

Yup, and banks are returning to high-risk securities, trading in debt-based products like collateralized loan obligations, just like they did leading up to the 2008 global financial crisis.

Bank: You should take out this loan you can’t afford to repay. Don’t worry, we’ll make it seem like a great idea.

Unqualified borrower: Ok, since you made it seem like a great idea.

Bank: Great! Hey, other bank, betcha this guy won’t repay this loan.

It’s not out of thin air, it’s out of your account, and everyone else’s too. They’re banking (heh) on most people not needing most of their money all at once. They keep a required reserve amount for people to actually withdraw. If all of the sudden everyone wants all of their money then that’s a run on the bank and it collapses.

No, it is actually out of thin air.

When a bank gives out a credit, that money is created on the spot, not drawn from somewhere.

There are rules as to how much money a bank is allowed to create, based on how much they actually have.

But no account of any kind is reduced by the amount they give out as credit.When a bank gives out a credit, that money is created on the spot, not drawn from somewhere.

Incorrect. Try starting your own bank and doing that. No other banks will do business with you and you’ll run out of money to give your borrowers.

This is how banks work.

You deposit 100 and I deposit 100, bank is required to keep 10 percent in cash (for example) that allows for 180 in loanable cash.

The bank loans out 180 dollars, now you have 100, I have 100 and someone else has 180, that money has been ‘created’ out of thin air.

The banks count on the fact that that me and you won’t both withdraw all of our money at once.

When banks finish the day, they actually check and see if they are within all of the margin limits that are required and do overnight loans from other banks to stay legal.

Look up fractional reserved banking.

bank is required to keep 10 percent in cash

Not correct. Your liabilities need to be sufficiently smaller than your assets. Capital reserves don’t need to be in cash.

someone else has 180, that money has been ‘created’ out of thin air

200 dollars went in. 180 dollars came out. 20 dollars stay in the bank. No dollars have been created.

Look up fractional reserved banking.

Look up solvency frameworks

Money hasn’t been printed, but for the bookkeeping, 3 individuals who have contributed a total of 200 dollars, have in their accounts 380 dollars.

When a bank loans your money out, as we are well aware, they don’t change the account in your balance. In order to do that, the dollar being loaned must be duplicated somehow. This is normal to how fractional banking works, and guidelines and requirements for how much specific money you need to maintain doesn’t change that.

The only way to change it is to switch to full reserve banking.

If a bank is able to loan out your money, without also removing it from your account, it is by nature created, the money is in two places at once.

Money hasn’t been printed, but for the bookkeeping, 3 individuals who have contributed a total of 200 dollars, have in their accounts 380 dollars.

Person A’s account: $100 Person B’s account: $100 Person C’s account: -$180

This does not add up to $380.

They don’t reduce your available balance because they’re constantly juggling the money around. But they’re not producing money out of thin air. They can’t loan more than they hold in deposits.

Yep. Just don’t borrow it, fuck em.

Unless you’re really rich, you have the choice between borrowing money from the bank, and paying rent to a landlord for your entire life.

Unless you’re moderately rich, you don’t even have that choice.If people could buy housing without needing to borrow money, the world would be a much better place.

While funny, and this is a the meme community, God it’s so much worse than that. Debt accumulated in a western style capitalist society is just how money exchanges hands. Your debt, the one that deeply affects your life, that can ruin your ability to make basic purchases and health care is a simple gamble for the rich, OUR debts.

Their debts are waved away, all because it makes more profits to forgive major mistakes when the other people are rich. I’m looking at you GM and Chrysler, I’ll never forget.

Edit: I forgot.

Wasn’t Ford the American auto company who didn’t have to be bailed out by taxpayers while GM and Chysler did?

Maybe. Listen, what I said was in the moment. You can’t blame me for being stupid on the internet lol.

You just need to be more careful.

I’ve never been wrong about anything online. How could that even happen?

Asymptotically Correct (Wrong in this instance)

doesn’t pay it back

2008 financial crisis

when your puny change in mortgage loan causes upwards of a billion dollars worth of

investmentsgambling to fall apartMy Student loans were sold before I even finished school.

Don’t even ask the question.

The answer is yes, it’s priced in.

Think Amazon will beat the next earnings? That’s already been priced in.

You work at the drive thru for Mickey D’s and found out that the burgers are made of human meat? Priced in. You think insiders don’t already know that?

The market is an all powerful, all encompassing being that knows the very inner workings of your subconscious before you were even born.

Your very existence was priced in decades ago when the market was valuing Standard Oil’s expected future earnings based on population growth that would lead to your birth, what age you would get a car, how many times you would drive your car every week, how many times you take the bus/train, etc.

Anything you can think of has already been priced in, even the things you aren’t thinking of.

You have no original thoughts. Your consciousness is just an illusion, a product of the omniscent market. Free will is a myth.

The market sees all, knows all and will be there from the beginning of time until the end of the universe (the market has already priced in the heat death of the universe).

So please, before you make a post on Reddit asking whether AAPL has priced in earpods 11 sales or whatever, know that it has already been priced in and don’t ask such a dumb fucking question again

{kind=link}